What Can You Expect?

When it comes to Social Security benefits, most people do not plan on it as their only source of retirement income. However, it has been and will continue to be an important retirement foundation for retirees across the country. The question people are asking themselves today is: What will this source of income look like in the future?

Why the Question?

Everyone from young professionals to those nearing retirement is wondering about the future of the Social Security System.

It is true, based on the numbers and without any governmental change to the current system, that the Trust Fund paying out Social Security benefits may be depleted by 2033. This is simply a matter of math, based on careful calculations of many actuaries who every year pore over a set of statistics to make assumptions for the next 75 years. These facts are reported each year in a document called the “Trustees Report.”

The Details

Starting in 2022, according to the 2013 Trustees Report, revenues and interest income alone will not be enough to cover total expenditures. The Trust Fund will then start to be tapped so that Social Security benefits can continue to be paid at the now projected current rates for beneficiaries. Said another way, the Federal Government will start to use the principal of the Social Security Trust Fund to supplement beneficiaries’ retirement checks. By the way, this is why the Trust Fund was created in the first place. Like any other saving account, it provides a shock absorber to the system. By 2033, reserves in the Trust Fund are projected to be gone. That’s the bad news.

Here’s the good news: the system will be far from bankrupt because Social Security tax contributions will keep coming in. These tax contributions are projected to cover up to 75 percent of the benefits due.

If these projections don’t improve due to economic and demographic trends, policymakers will likely have to make some changes to the program before 2033 to ensure that all scheduled benefits can be paid. Adjusting the program is something that Congress has done several times during the 79-year history of Social Security program.

There are a number of proposed solutions that are floating around to actually address the projected deficit in Social Security. Some of the ideas are lifting the cap on earnings subject to Social Security contributions, increasing the Social Security Tax contribution rate, and/or raising the retirement age.

Most likely, the system will be “fixed” with a combination of benefit adjustments and revenue increases. Keep in mind that in the past, when Congress made changes to Social Security, they were implemented gradually over a long period of time to prevent major shocks to the system. These changes will most likely impact younger workers rather than workers nearing retirement.

What about Me?

In the end, how much you get has less to do with government formulas, since those are out of your control, and more to do with you — namely your retirement age and when you decide to file for benefits.

How Much Will I Get?

It depends. Everyone is different. To find the answer you need to consider four major variables: your earnings history, marital status, age and longevity.

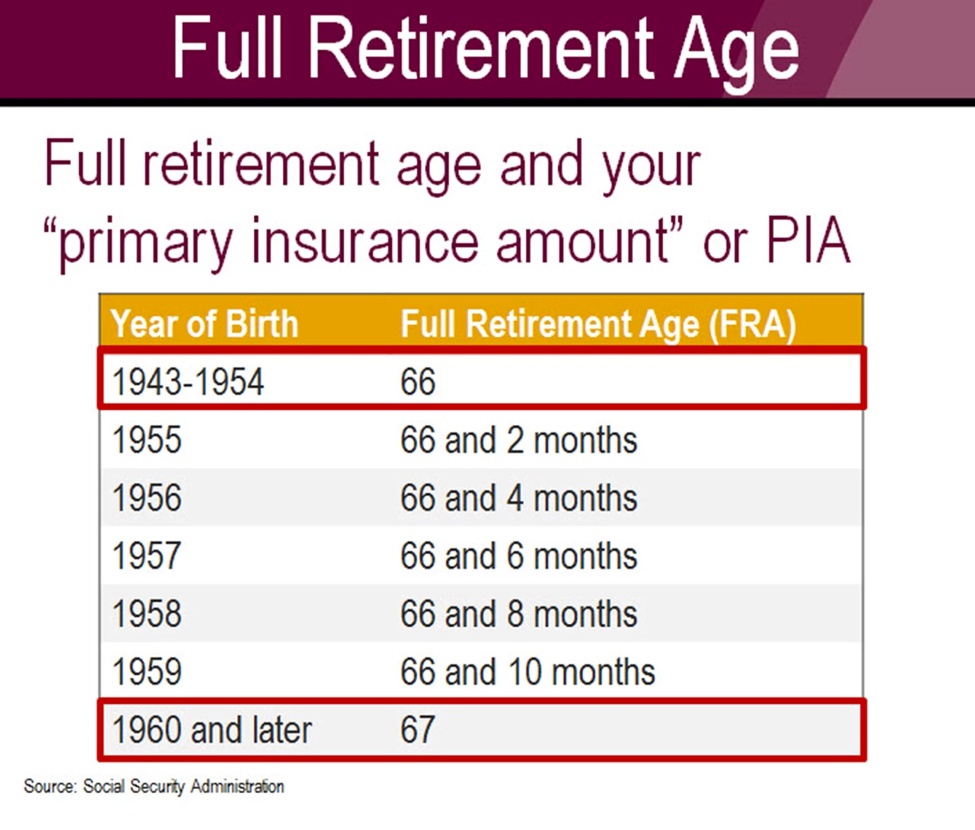

If you don’t know what your benefit projection for your full retirement age is, remember that you can get a report from the Social Security Administration online. Visit www.ssa.gov for more details. In addition, it’s important to know your full retirement age (FRA), which is determined by the year of your birth.

Does My Current Age Matter?

Only to the extent that the longer you wait to collect your benefits, the larger your monthly benefit will be.

You will need to decide whether to begin collecting at the earliest possible age (62) or at the latest age (70). When you start collecting is up to you. However, the government makes you wait until full retirement age in order to get your “full” retirement payout. Taking benefits early can reduce the monthly payments by up to 25 percent. If your full retirement age is 66, taking benefits at age 70 can increase the monthly payments by up to 32 percent, due to delayed retirement credits. As you can see in the graphic, the full retirement age for everyone born between 1945 and 1954 is 66. If you were born after 1954, the full retirement age gradually increases to 67.

The Answer to the Million-Dollar Question

While congressional leaders ponder and debate the next steps and necessary changes in the evolution of the Social Security program, you may want to take a few steps of your own:

- Meet with a Financial Professional who can help you with full retirement age projections, which ultimately will help you determine how and when to take benefits.

- Discuss the suitability of tax-advantaged vehicles, such as Roth IRAs and annuities as supplements to Social Security income.

- Consider permanent life insurance. When a spouse dies, for example, life insurance death benefits can help offset the loss of Social Security income.

While we don’t know for certain how Social Security will evolve in the future, one thing is clear: Much of your future income for retirement will depend on decisions you make now. By planning ahead for retirement and assessing what income sources you’ll have, you can be better prepared for the next chapter in your life.

For more information on Social Security retirement benefits, visit the Social Security Administration at www.ssa.gov.